Introduction

A Roth conversion is a process of transferring funds from a traditional retirement account like a Traditional IRA into a Roth IRA. The amount converted is subject to income tax in the year of the conversion, but once in the Roth IRA, future earnings and withdrawals are tax-free. The intent of the conversion is to reduce future tax payments by paying tax early at a lower rate, anticipating a higher future tax rate.

The conventional approach to Roth conversion assumes that it is beneficial only if the tax rate at withdrawal is expected to be higher than at conversion. However, this criterion has limitations, as it overlooks the fact that a Roth conversion can still make gains even if the withdrawal tax rate is slightly lower than the conversion rate, due to tax drag from reinvested required minimum distributions (RMDs).

In a real-life conversion, the effect of tax drag will be small, so that even in the best-case scenario, the gains may be minimal. However, it can reduce the potential losses from a negative delta (when the withdrawal tax rate is lower than the conversion tax rate) to some extent. While there are theoretically favorable tax brackets in which to make conversions, the constraints and lack of control in reaching them make Roth conversions complex and challenging.

Those who consider or recommend Roth conversions often argue that anticipated future tax rate increases make it urgent to convert as soon as possible to avoid higher taxes later. Additionally, they believe that completing Roth conversions now will protect them from potential changes in tax laws. However, numerous precedents and recent developments challenge this assumption.

Mechanisms of Tax Drag

Understanding tax drag in the context of Roth conversion requires analyzing the financial implications of not converting a Traditional IRA. If the Traditional IRA is left unconverted, it will release RMDs annually after the account holder turns 73. Those who do not need these RMDs for living expenses often reinvest them in taxable accounts rather than depositing them in bank accounts. The performance of the Roth IRA is compared against this counterfactual (an unconverted Traditional IRA + reinvested RMDs), as discussed in the 2023 study by McQuarrie & Dillelio.

The reinvestment of RMDs creates taxable consequences, such as receiving dividends and interest and realizing gains. In contrast, the only tax payment in a Roth conversion is the tax paid upon conversion, and the absence of these taxes from reinvested RMDs gives a Roth IRA superior compounding power.

Conventionally, it is believed that a Roth conversion would be successful only when the conversion tax rate is lower than the tax rate individuals pay to make withdrawals from the Traditional IRA, particularly after the start of RMDs. However, due to the effect of tax drag, the conversion can result in gains even when the withdrawal tax rate is slightly lower than the conversion tax rate.

Nevertheless, in the context of Roth conversion, tax drag will be minimal. This is because Roth conversion is intended to be treated as a financial wealth (wealth on paper) rather than a consumption wealth (wealth to be expended). Making withdrawals of the converted funds will result in lower gains or losses due to the diminished compounding power from the reduced principal amount.

Since the Roth IRA should ideally remain untouched, its counterfactual is also treated in the same manner, creating minimal tax consequences, potentially resulting in only 0.3% tax drag on a taxable account. Assuming a 10% rate of return on investments from an all U.S. equity portfoio, only a small portion of the return—approximately 20% from dividends and interest—is taxed. If these are taxed at a 15% rate for dividends and interest, the effective tax drag is just 0.3% (10% × 20% × 15%).

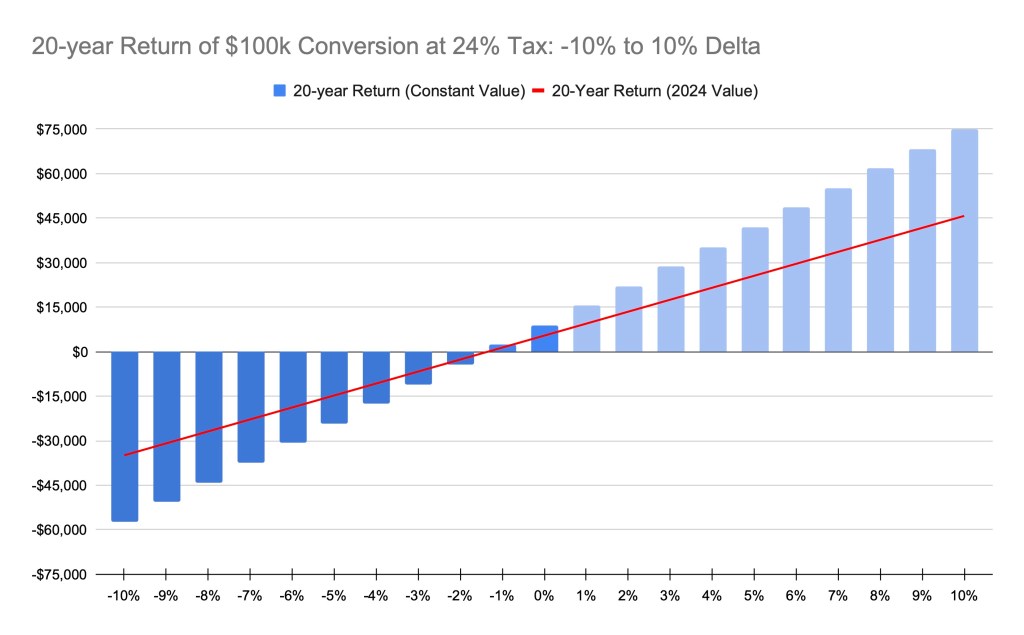

Graph 1 illustrates the 20-year performance of a Roth conversion. The exercise converts $100,000 when the retiree is 72 years old, at a 24% conversion tax rate. The investment inside the Roth IRA is allocated entirely to U.S. equities, assuming a 10% annual growth rate. This conversion is compared with the counterfactual, where the unconverted Traditional IRA releases Required Minimum Distributions (RMDs) starting at age 73. These distributions are reinvested in a taxable account, also in U.S. equities with the same rate of return, and generate dividend and interest income subject to a 0.3% total tax rate. It creates a small tax drag, giving the Roth IRA a performance edge.

The graph compares 20-year profits across different deltas, ranging from -10% to 10%. For example, if the conversion tax rate is 24% and the withdrawal tax rate is 22%, the conversion delta is -2%. Due to the tax drag, there are small gains even when the delta is zero or -1%, and losses at higher negative deltas are mitigated.

The relevant deltas from real-life conversions range from -10% to 0%. A large negative delta of -10% can occur, for example, when converting at the 22% tax tax rate, and the withdrawal tax rate falls to 12%. Conversely, the best-case scenario results in a delta of 0%, where the conversion and withdrawal tax rates will be the same, and there will be modest gains due to small tax drags. As discussed later, converting a sizable amount and achieving a positive delta will be highly challenging. This exercise indicates that one can expect only a modest gain from the conversion. Losses may be negligible up to a -4% delta, but they can become substantial at a -10% delta.

Despite the potentially large loss, it is important to note that the Roth IRA’s losses are relative to the unconverted counterfactual. In absolute terms, even if the conversion experiences a negative 10% delta, it will still be increasing in value, though more slowly than if not converted. If the proportion of the converted amount is small relative to one’s overall assets, the loss will not be significant.

Timing for Conversion

The timing of the conversion greatly influences its outcome, so it is crucial to carefully consider when to execute it. The best time for individuals to make a conversion is after retiring (if they plan to retire) but before starting to take Required Minimum Distributions (RMDs) and possibly Social Security, to maximize the amount of the conversion. For most individuals, this would be between ages 65 and 72. Converting during this period allows for more accurate estimation of future income and tax rates compared to when they are still working.

Making a conversion while working is disadvantageous, especially for high-income individuals. Earned income can add hundreds of thousands of dollars to taxable income, limiting the amount that can be converted. Moreover, to remain in high tax brackets (32%, 35%, and 37%) after retirement, one would need tens of millions of dollars in non-retirement investment accounts and other passive income sources. When still accumulating financial assets, it is challenging to accurately estimate how much will be saved by the time RMDs are required. For these reasons, it is generally better to wait until retirement before making a conversion.

An additional reason not to convert early, such as several years before retirees are required to start taking RMDs, is that the unconverted Traditional IRA grows tax-deferred, and the comparison between the Roth conversion and the Traditional IRA will only be meaningful once the retiree begins receiving RMDs, which are taxed after age 73. Unless they plan to convert multiple times, it may be prudent to narrow the gap between the timing of conversion and withdrawal.

For this constraint, the period during which the Roth IRA outperforms the counterfactual scenario is limited after age 73, with this period typically lasting about 20 years, depending on life expectancy.

Suitable and Unsuitable Tax Rates for Conversion

Roth conversions should be done toward the end of the year, when one has a good estimate of total income for the year. Therefore, the conversion amount will be added last to calculate the total income and will mostly be taxed at the marginal tax rate.

If one were to make a Roth conversion, it is important to ensure that the conversion amount, which will be counted as taxable income, does not fall within tax brackets where the next lowest one is much lower, with some exceptions. The current marginal tax brackets are as follows: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. The following tax rates—22%, and 35%—have the next lowest bracket that is more than several percentage points lower. For example, the next lowest bracket for the 22% rate is 12%, which is 10% lower.

The risk of converting in brackets such as the 22% rate is that if the withdrawal tax rate drops to the 12% bracket, there will be a -10% delta, and the conversion will incur a large loss compared to the counterfactual (an unconverted Traditional IRA and reinvested RMDs in a taxable account). The same applies to conversions in the 32% bracket, in which if the withdrawal tax rate drops to the 24% bracket, there will be an -8% delta. Such risks for a large negative delta increase if retirees’ incomes, including Social Security, place them close to the floor of these unfavorable tax rates before conversion, leaving them with little cushion between the lower rate after conversion.

However, if retirees’ incomes are near the ceiling of the 22% bracket before Social Security and RMDs, a conversion could still be done. Being close to the ceiling of one tax rate is similar enough to being near the floor of the next highest tax bracket in the context of Roth conversion. Therefore, as in the case of the 22% bracket, they can potentially convert into the 24% tax bracket. This conversion strategy may place retirees in the 24% withdrawal tax bracket due to the additional income from Social Security and RMDs after conversion. Most of the 22% bracket itself, along with these additional incomes, becomes a cushion, making it difficult for the withdrawal tax rate to fall below the 22% bracket. However, such a maneuver requires careful review.

With less risks invovolved, a similar strategy can be employed for the 10% tax bracket if retirees find themselves in it before Social Security and RMDs. Their withdrawal tax rate may rise to the 12% bracket due to the low ceiling for this bracket: $24,662 for single filers and $49,323 for married couples filing jointly in 2025, after factoring in the standard deduction. For such individuals, there may be an opportunity to convert near the ceiling of the 12% bracket, and their withdrawal tax bracket may remain the same or drop to the 10% at worst.

From the perspective of minimizing the risks of experiencing a negative conversion delta, the 12%, 24%, 35%, and 37% tax brackets are technically favorable for conversion. For example, by converting at the 12% tax rate, even if income falls after conversion to 10%, the -2% delta will produce only a modest loss over time. The same applies to converting at the 24% tax rate, where the next lowest bracket is the 22%.

Although such conversions can be done theoretically, the probability of being in a tax bracket of 22% or higher in retirement is low for the vast majority of individuals.

Tax Brackets and Distributions Across Different Age Groups

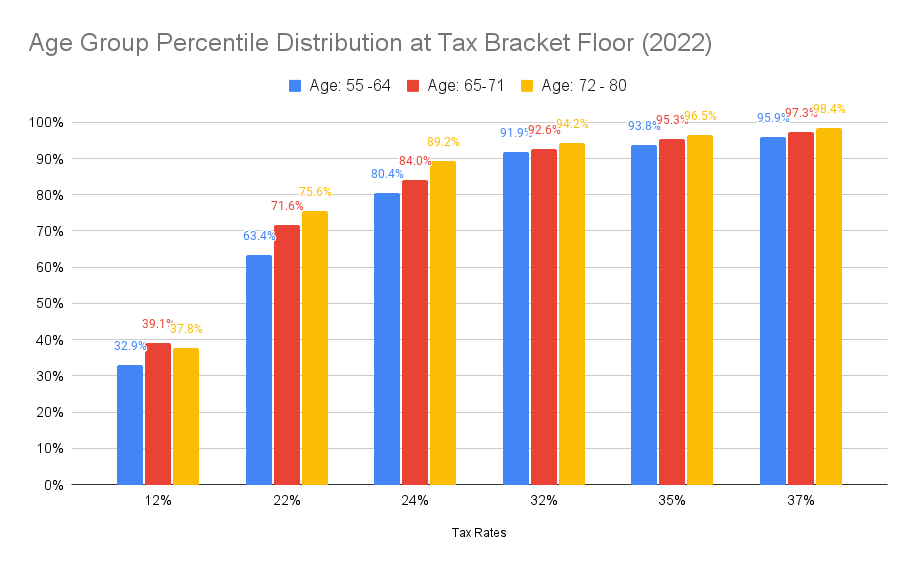

Graph 2 shows the percentage of people in different age groups whose income reached the floor of each tax bracket for married couples filing jointly, after accounting for standard deductions in 2022. The first group, aged 55–64, represents individuals primarily in their working years. The second group, aged 65–71, includes those approaching the age required to begin RMDs (age 72 in 2022). The third group, aged 72–80, comprises individuals who are required to start taking RMDs.

This data presented in the webiste Personal Finance Data, and originally taken from the Survey of Consumer Finances (SCF), suggests that the older the indiviuals are, the less likely they are to remain in the same tax bracket after the conventional retirement age of 65. Even in the 22% tax bracket, at a relatively low tax bracket, although more than 35% of people surveyed earned at or above it between the ages of 55 and 64, less than 30% earned at this level for those aged 65 to 71, and less than 25% belonged to this bracket for those aged 72 to 80.

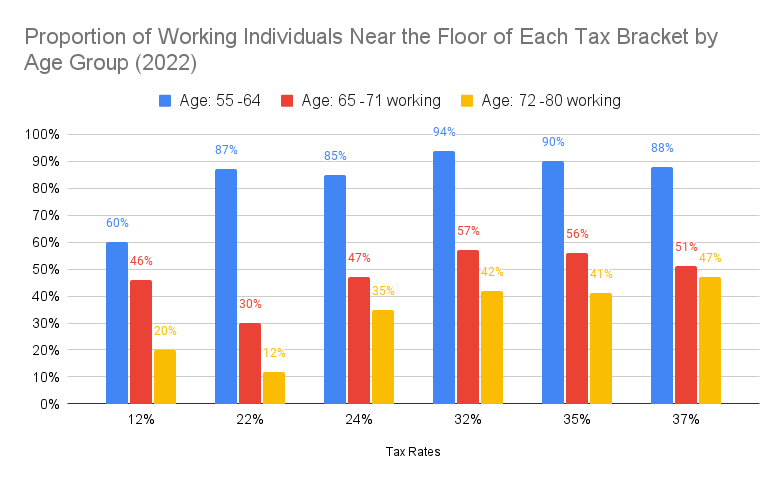

Furthermore, a significant portion of individuals in the age group of 72 to 80 who belonged to high-income tax brackets still had earned income from work. For example, Graph 3 shows that, at the highest marginal tax rate of 37%, individuals with an income of $673,750 (after factoring in the standard deduction for married filing jointly in 2022), 47% of the people in this age group surveyed were still working. Since 1.6% of the people earned income at this highest tax bracket, approximately half—only 0.8%—had incomes at this tax rate without any income from work. The samples taken in the SCF survey are skewed toward higher incomes, so the actual number could be even smaller.

In contrast to higher tax brackets, a much smaller proportion of individuals in lower tax brackets had earned income from work. Among those aged 70 to 80, only 20% of individuals in the 12% tax bracket were working, while just 12% of those in the 22% tax bracket were employed. Considering that only less than 30% of individuals approaching RMD age belonged to the 22% bracket or higher, the 12% bracket is likely to be a common marginal tax rate after retirement for many individuals considering a Roth conversion.

Assets Required for Different Tax Rates

Most individuals retire for various reasons, such as personal factors and the physical demands of work. When they no longer have earned income, their income sources, such as Social Security, RMDs, and investment income from non-retirement accounts, determine their tax rate. Starting from the relatively low 22% tax bracket, the amount of assets needed to generate income that places retirees in these tax rates can become high for the majority of retirees.

Even for the 12% tax bracket in 2025, it will take a significant asset of close to $1.8 million in non-retirement account assets with a 3% portfolio income rate to reach the floor of this bracket before receiving Social Security and RMDs. If the taxable portion of the Social Security income were counted to calculate the income before conversion, much less financial assets would be required to reach the floor of this tax bracket.

| Tax Bracket (2025_Married Filing Jointly) | Tax Bracket Floor + Standard Deductions | Portfolio Balance That Generates This Income at 3% Income Rate |

| 12% | $53,201 | $1,773,367 |

| 22% | $124,301 | $4,143,367 |

| 24% | $231,051 | $7,701,700 |

| 32% | $413,901 | $13,796,700 |

| 35% | $517,451 | $17,248,367 |

| 37% | $761,201 | $25,373,367 |

However, starting from the 22% tax bracket and beyond, significant financial assets, such as non-retirement investment accounts and other passive income sources, are required to reach these brackets. In 2025, it will take over $4.1 million in non-retirement investments at a generous 3% income rate to reach the floor of the 22% tax bracket before accounting for Social Security and RMDs. To reach the 24% marginal rate, it will require over $7.7 million, and more than $25 million will be needed to reach the 37% marginal tax rate. Even with RMDs and the taxable portion of Social Security, millions in financial assets will still be necessary.

Low Probability of Facing High Tax Rates in Retirement

Although individuals considering a Roth conversion may expect that their tax rate during retirement may remain as high as while they were working, research from Boston College shows that most retirees pay little to no taxes after retirement. Four in five retirees pay nearly 0% in taxes, while the top 20% pay an effective tax rate of 11% on their retirement income. The top 1% pay 23% on their retirement income.

The reason most retirees pay almost no taxes after retirement is that their primary source of income is Social Security. At most, 85% of Social Security income is included in taxable income once certain thresholds are crossed: $34,000 for single filers and $44,000 for married couples filing jointly in 2025. Research suggests that most retirees have not saved significant non-retirement assets that can generate this level of income.

Although people considering a Roth conversion may be above-average savers, they might be greatly overestimating their future incomes. Those who can reasonably expect hundreds of thousands in income at an age when most individuals are retired may be successful business owners or have other sources of lucrative passive income, and they are outliers. For most people, accumulating tens of millions in financial assets is extremely challenging, as it requires sustained high income over a few decades while adhering to a modest lifestyle. This approach necessitates viewing assets primarily as wealth on paper rather than as something used for consumption.

Moreover, tax brackets are adjusted annually for inflation. This adjustment means that a higher income is required each year to remain in the same tax bracket. As a result, it becomes highly challenging for individuals without earned income to move into a higher tax bracket and achieve a positive delta.

Additionally, to increase taxable income, retirees may need to adjust the composition of their non-retirement accounts. A prudent asset allocation for a retiree typically includes a significant portion of fixed income instruments, with a large share in tax-free bonds. However, to remain in the same tax bracket as the conversion, they may need to replace the tax-free bonds with riskier, high-yield taxable bonds or realize capital gains. Since the purpose of a Roth conversion is to reduce future tax payments, increasing taxable income to make the Roth conversion viable conflicts with its original intent.

Arguments Against Roth IRA Immunity from Tax Hikes

Those who advocate for Roth conversions believe that new tax laws will increase tax rates and that Roth conversions will shield them from such changes. However, Roth IRAs may not be immune to changes that affect Traditional IRAs and other types of accounts. For example, the elimination of the stretch IRA under the SECURE Act in 2019 affected both inherited Traditional and Roth IRAs. This illustrates that provisions we take for granted can be altered by Congress, and they could make changes that were once considered unthinkable.

An example of this potential surprise is that Democratic legisaltors were considering taxing unrealized gains. While the defeat of the Democrats in the 2024 presidential and congressional elections means that such plans will not be legislated in the coming years, it does not mean they cannot happen in the future. If they do, it would not be surprising if a law to tax gains in Roth IRAs were also proposed.

Another reason Roth IRAs may not be spared from changes in tax laws is that the government typically seeks to prevent taxpayers from exploiting loopholes in the system. If such a loophole exists, it is likely to be closed. For example, prior to 2015, one spouse, such as a husband, could use the “file and suspend” strategy in Social Security, where he would file for benefits but choose to suspend the payments instead of receiving them. This allowed his benefits to grow until he reached full retirement age or age 70. Meanwhile, his wife could claim half of his suspended Social Security benefit while her own benefits continued to grow. This arrangement allowed the wife to receive spousal benefits while both spouses’ benefits increased, which they could later claim to maximize their payments. However, this loophole was closed in 2015.

If the IRS concludes that the agency is losing money from Roth conversions, they could end this practice. However, the reality of Roth conversions is that it is difficult to easily make large profits, and it is easy to experience a large negative delta, where the withdrawal tax rate is several percentage points lower than the conversion tax rate.

Conclusions

Considering these factors, it is plausible that Roth conversion was designed to allow the government to collect taxes sooner before RMDs start, rather than later, to help cover increasing budget deficits, making the IRS the overall winner while the majority of conversions fail to see any gains.

If there is certainty of a future tax increase, such as when a new law is passed, there may be a small window of opportunity to make a conversion at a lower rate before the new law takes effect. However, provisions that affect Roth IRAs may limit or prevent such an opportunity.

Due to the projected tax policy of the new Republican administration, which favors a low-tax environment, a large proportion of those who have already made Roth conversions and will be making RMDs in the coming years may experience losses, especially if they converted while working and belonged to a marginal tax rate of 22% or higher. What makes a Roth conversion complex and challenging is that, while it can theoretically generate gains if certain conditions are met, it is difficult to know with certainty what the future holds, both from personal and legal perspectives. Changes in these unpredictable factors can significantly affect the outcomes.

Roth conversion can technically make gains thanks to the effect of tax drag. However, each individual’s circumstances, such as their asset levels, asset composition, and where their income falls within a tax bracket, vary significantly. This makes Roth conversions complex and requires a thorough and personalized assessment. After such an evaluation, while it may be suitable for some to make a conversion, in many cases, it may ultimately not be advisable.

Schedule a call with me here.

The information provided in this blog post is for educational purposes only and does not constitute financial advice. It is not intended as a recommendation to buy, sell, or hold any financial product, and I do not promote any organizations.